A Saudi decision to indefinitely delay an initial public offering (IPO) of five percent of the Saudi Arabian Oil Company or Aramco, the Saudi state-owned oil company, has further dented investor confidence and fuelled debate about Crown Prince Mohammed bin Salman’s ability to push economic reform. It has even prompted speculation that his assertive policies, including the Kingdom’s ill-fated military intervention in Yemen, harsh response to Canadian human rights criticism and failed Saudi-United Arab Emirates-led diplomatic and economic boycott of Qatar, could dampen his prospects of eventually ascending the throne.

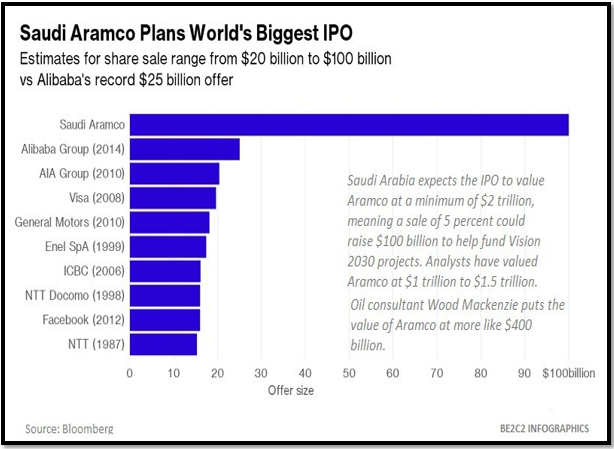

No doubt, Prince Mohammed touted the IPO, projected as the world’s largest with a US$ 100 billion price tag, as a litmus test of the Kingdom’s willingness to diversify and reform its economy. There is also little doubt that Prince Mohammed may have been too ambitions in his US$ 2 trillion valuation of Aramco, misread market conditions, and underestimated political and bureaucratic resistance to transparency requirements associated with a public offering of what The Economist once dubbed “the world’s biggest, most coveted and secretive oil company.”

As a result, the indefinite delay, ordered by King Salman in his second intervention this year to curb the Crown Prince’s policies, was widely perceived as yet another failure of a young, inexperienced, and often impetuous crown prince. Yet, it could prove to be a blessing in disguise given that international financial markets currently value national oil companies at a steep discount. The delay, moreover, does not leave the Kingdom without options, including a long suggested private equity sale.

The Beginning of the End?

Saudi oil minister Khalid Al Falih was emphatic in his insistence that the Kingdom remained committed to an Aramco initial public offering in his August 2018 announcement that the IPO had been indefinitely delayed. “The government remains committed to the IPO of Saudi Aramco at a time of its own choosing when conditions are optimum,” Al Falih said in a statement. (1) The statement put an end to speculation about the timing and fate of the offering that had been originally planned for 2017. To be fair, Al Falih had long maintained that the Kingdom was not bound by a timetable. "Timing isn’t critical for the government of Saudi Arabia," he said more than a year before the final postponement. (2)

The disconnect between Saudi imperatives and the expectations of Western governments and financial markets who repeatedly focussed on unmet Saudi time indications of the IPO rather than broader policy statements fit a pattern of misperceptions that dates back to the days of Aramco’s founding by US oil companies that at the time had a major stake in what was then a US registered entity, the Arabian American Oil Company when American oilmen repeatedly underestimated their Saudi counterparts and misread their intentions. (3)

|

| [Bloomberg] |

Western analysts, in what could be a similar disconnect, have suggested that the delay could prove to be the straw that breaks the camel’s back. “MBS is not a reformer and nor is he a strongman since, with a stroke of a pen, his father can alter the succession and strip him of his power. That may happen soon, given the growing clamour from angry princes. Perhaps that is why MBS slept on a heavily guarded yacht moored off Jeddah all summer,” said author Michael Burleigh, referring to Bin Salman by his initials. (4)

The analysts position the delay of the IPO as the last of a string of Crown Prince Mohammed bin Salman’s policy fiascos, including the ill-fated 3.5-year-long war in Yemen that has significantly damaged the Kingdom’s image and projection of itself as a military power; (5) a crude attempt to control Lebanese politics by arm twisting prime minister Saad Hariri to briefly resign; (6) an out-of-proportion almost hysteric response to Canadian human rights criticism; (7) an asset and power grab dressed up as an anti-corruption campaign; (8) and a crackdown on critics of any stripe.(9)

The fact that Bin Salman’s father, King Salman, had by ordering the delay of the IPO, (10) intervened for the second time within a matter of months to curb his son’s policy initiatives fuelled speculation that the move may be the beginning of his son’s end. Salman had stepped in earlier to put an end to Bin Salman’s tiptoeing around condemning US President Donald J. Trump’s recognition of Jerusalem as Israel’s capital. (11)

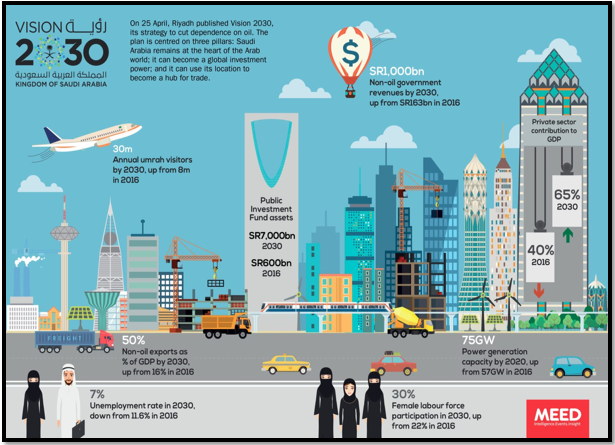

Bin Salman’s drawbacks notwithstanding, King Salman, an ailing octogenarian, may not want his legacy to be admitting to appointing a son as his heir who dragged the ruling Al Sauds’ kingdom down. More likely is that Bin Salman will quietly be put on a tighter leash. The delay of the IPO, positioned as the crown jewel of Vision 2030, Bin Salman’s economic and social reform program, (12) will, moreover increase pressure on him to deliver on promises of jobs and greater opportunity.

To do so, Bin Salman will have to redress the balance sheet of his three years in office that so far is heavy on failures and short on successes that largely involved low-hanging fruit like the lifting of a ban on women’s driving and granting of greater social and professional opportunities but have stopped short of abolishing, for example, male guardianship of women. That inevitably will require initiatives that restore confidence in his ability to deliver irrespective of if or when a stake of Aramco is publicly or privately sold.

|

| [MEED] |

A Blessing in Disguise?

In the ultimate analysis, the delay of the IPO of Aramco, the world’s largest private oil company with estimated hydrocarbon reserves of 261 billion barrels or ten times those of ExxonMobil and one of the world’s lowest production break even points, could prove to be in Bin Salman’s string of failures the one blessing in disguise. No doubt, an IPO would have raised a substantial amount even if it likely would have been below Bin Salman’s unrealistic expectation of a US$100 billion yield and it would have made good on the crown prince’s promise of a more transparent, more user-friendly business environment.

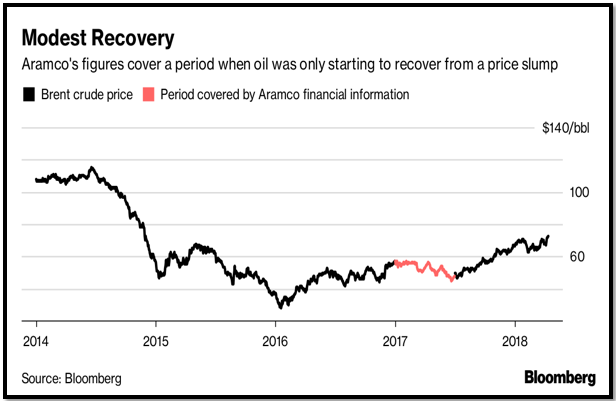

The delay, however, at least temporarily resolves a number of technical or more principle issues associated with the public offering. The most immediate was timing given that the current market climate does not favour national oil companies.

“National oil companies probably have much deeper reserves than the international oil companies, and yet they still don’t get massive premium valuations; they get discounted valuations. It makes a huge amount of sense because if they ultimately destroyed value by going too quickly or if they weren’t able to realise the prices they’d like to see, then quite frankly it makes sense for them to delay things a little bit,” said Hootan Yazhari, head of Middle East, North Africa and frontier markets at Bank of America Merrill Lynch. (13)

The delay also shields the Kingdom and Bin Salman from embarrassment with markets likely to put Aramco’s value at far below the crown prince’s US$2 trillion expectation. Moreover, Saudi Arabia’s effort to raise funds to finance reforms and fill the coffers of its Public Investment Fund (PIF), the Kingdom’s sovereign wealth fund envisioned as the motor of economic diversification, was not wholly dependent on an IPO that risked further dividing the ruling family as well as powerful parts of the bureaucracy. Many in the family and bureaucracy were believed to be opposed to the move for multiple reasons, including the associated transparency requirements that could expose profits reaped by the ruling family, a belief that it amounted to a rollback of Saudization of Aramco and a return of the Kingdom’s foremost asset to non-nationals and fears that the process could give Bin Salman the kind of control of Aramco that Saudi rulers have eschewed for decades in their bid to maintain the company as the mainstay of their rule. Some of the opponents’ arguments also complicated prospects for a possible private equity sale to a Chinese state-owned entity.

The opposition’s success in delaying the IPO could, however, prove to be a double-edged sword. Aramco achievements were for the better part of a century vested in the fact that it has been able to operate on principles of American corporate management even after the Saudis bought out the American shareholders in the 1980s and in 1988 moved Aramco’s incorporation from Delaware to the Kingdom. While much of the Saudi leadership understood that those principles guaranteed it the cash flow and geopolitical influence it needed to maintain its grip on power, Aramco was largely able to fend off occasional attempts by the government to gain direct control of the company’s finances rather than depend on its tax, royalty and dividend payments even if was forced to make minor concessions. (14) Those concessions are reflected in the fact that Aramco owns a string of soccer fields, acts as project manager for some of the government’s non-oil developments, and operates a hospital system that services close to 400,000 people.

|

| [Bloomberg] |

Nonetheless, the guiding principle that ensured Western-style commercial management threatens to be violated as Bin Salman looks at alternative sources to compensate for the immediate loss of the US$100 billion Aramco IPO windfall. A US11 billion syndicated bank loan secured by the Kingdom in September 2018 accounts for only 11 percent of the loss. (15) Bin Salman is counting on raising and additional US$70 billion by engineering the acquisition by Aramco of the 70 percent stake in petrochemicals, minerals and metals producer Saudi Basic Industries Corp or SABIC from the Public Investment Fund. Aramco’s management, in an effort to fend off Bin Salman’s attempt to use the company as a fundraising vehicle, has argued that the government was overpricing SABIC and demanded that the price be discounted by up to 25 percent. (16) A sale below SABIC’s market price would not only inject less capital into the sovereign-wealth fund, but also drive down the company’s shares listed on Tadawul, the Saudi stock exchange with a market capitalization of US$95 billion. “The prized assets of the state, like Aramco and SABIC, should not be used as cash cows to feed the experiments of the PIF’s outward investment strategies,” cautioned political economist Karen E. Young. (17)

To be fair, an acquisition of SABIC would have in principle some merit given Aramco’s bet on the future that includes a belief that the creation of increased more demand for crude in the chemical sector can counter expectations that fossil fuels are in decline. To create demand, Aramco is developing technologies that will help convert crude directly into chemicals without refining it first into lighter products such as naphtha, a process that could costs by some 30 percent. Using oil as feedstock would “secure a large and reliable home for our future oil production,” said Aramco CEO Amin Nasser. (18)

Nevertheless, the indefinite delay of the IPO was bound to have serious consequences with or without a compensatory acquisition of SABIC. Rating agency Moody’s Investor Service warned that the Kingdom’s significant reliance on debt would increase liability risks and exert negative pressure on its credit profile. "The postponement of the IPO implies that the economic diversification envisaged by the government will either need to be scaled back or financed by higher direct or indirect public-sector debt issuance," Moody's said. (19)

The Kingdom’s problems are compounded by the fact that continued uncertainty about the fate of the Aramco IPO and Bin Salma’s broader reform program has prompted capital to head for the exit. JP Morgan estimated that capital outflows of Saudi residents in Saudi Arabia would be US$65 billion in 2018 or 8.4 percent of GDP, admittedly less than the US$80 billion last year but nonetheless a continuous bleed. Similarly, Standard Chartered reported US$14.4 billion in outward portfolio investment into foreign equities in the first quarter of 2018, the largest surge since 2008. “This flight signals the dimming of the optimism surrounding Crown Prince Mohammed bin Salman’s Vision 2030 economic plan,” Young said. (20)

If the Aramco IPO in Bin Salman’s vision was in part intended to promote transparency in Saudi Arabia and convince foreign investors that the Kingdom was rolling out an environment friendly to investors and the conduct of business, its indefinite delay sends a very different message. “Whether…foreign enterprises will risk their own capital in Saudi ventures…remains to be seen. The failure of the Saudi Aramco IPO has highlighted the mismatch between the needs of foreign investors and Saudi Arabia’s current investment environment,” said Stephen Grand, executive director of the Atlantic Council’s Middle East Strategy Task Force. (21)

Ironically, Aramco, as long as it was actively pursuing an IPO, Bin Salman a degree of cover for his repression of all dissent and his detention last year of hundreds of prominent businessmen, serving and former officials, and members of the ruling family in a power grab and asset shakedown dressed up as an anti-corruption campaign by positioning the sale of a stake in the company as an effort to enhance transparency. “I believe it is in the interest of the Saudi market, and it is in the interest of Aramco, and it is for the interest of more transparency, and to counter corruption, if any, that may be circling around Aramco,” Bin Salman said when he first suggested a public offering. (22)

External factors making a listing of Aramco shares in either New York or London, Bin Salman’s preferred exchanges because of their positioning among investors and the associated political benefits, difficult contributed to the IPO’s indefinite delay. Lawyers advising Bin Salman and Aramco pointed out that a listing on the New York Stock Exchange would potentially make Aramco liable to claims of victims of the 9/11 attacks on New York and Washington. Fifteen of the 19 perpetrators were Saudi nationals. US District Judge George Daniels in New York agreed in March to allow a class action suit filed on behalf of 1,500 injured 9/11 survivors and 850 family members of fatal casualties, (23) alleging that Saudi Arabia “knowingly provided material support and resources to the al Qaeda terrorist organization and facilitated the September 11th attacks.” The suit was filed under a bill passed by the US Senate in 2016, Justice Against Sponsors of Terrorism Act (JASTA), that allows civil lawsuits by victims of "international terrorism" to proceed in US courts against sovereign states. (24)

A bipartisan proposal in Congress to subject oil producers to US anti-trust laws that would allow Saudi Arabia and other members of the Organization of Oil-Exporting Countries (OPEC) to be sued if it were believed to have manipulated the market by colluding to control supply further clouded prospects for a US listing. (25) To prevent the bill, the No Oil Producing and Exporting Cartels Act, or NOPEC, from being tabled, Saudi Arabia hired Ted Olson, a high-powered solicitor general during the George W. Bush administration. (26)

A listing in London became problematic after the Investment Association, a fund manager lobby group, accused a British financial markets regulator, the Financial Conduct Authority (FCA), of watering down its rules to attract the Saudi IPO. (27) The complaint prompted the chairs of parliament’s Treasury and Business Select Committees to raise the issue, making it less likely that Aramco would be able to evade the kind of transparency issues associated with a listing on Western stock exchange. (28)

Conclusion

The indefinite delay of the Aramco IPO has dealt a boy blow to Saudi Crown Prince Mohammed bin Salman’s efforts to reform and diversify the Kingdom’s economy. It has also further dented foreign investor confidence, a pillar of Bin Salman’s reform effort. The crown prince’s effort to compensate for the loss of expected proceeds of up to US100 billion from the sale has forced him to look for funds elsewhere. His proposed acquisition by Aramco of a majority stake in petrochemicals giant SABIC threatens to undermine the managerial independence of the oil company, the rock bed of Saudi rule since the Kingdom was founded in 1932.

The delay of the IPO is nonetheless not all bad news even if it has called into question the future of Saudi reform and even sparked speculation about Bin Salman’s future. Bin Salman is not left without options. The Kingdom continues to enjoy access to international financial markets and retains the option of a private equity sale. Moreover, discounts of national oil companies by financial markets favour a delay of the IPO.

That does not necessarily shield Bin Salman. He may nevertheless be down, but he is not out. The delay, however, makes it all the more imperative for Bin Salman to meet expectations of a predominantly young Saudi population by delivering job creation and enhanced economic and social opportunity. That could be a tough nut to crack in the absence of domestic and foreign investor confidence in the crown prince’s ability to deliver.

Will a Saudi Aramco IPO ever happen? | Inside Story [VIDEO]

(1) Jennifer Gnana, Saudi Arabia 'fully committed' to Aramco IPO, oil minister says, The National, 23 August 2018, https://www.thenational.ae/business/energy/saudi-arabia-fully-committed-to-aramco-ipo-oil-minister-says-1.762866

(2) Javier Blas and Francois De Beaupuy, Saudi Oil Minister Says Timing of Aramco IPO ‘Isn't Critical,’ Bloomberg, 21 June 2018, https://www.bloomberg.com/news/articles/2018-06-21/saudi-oil-minister-says-timing-of-aramco-ipo-isn-t-critical

(3) Ellen R. Wald, Saudi Inc. The Arabian Kingdoms Pursuit of Power and Profit, New York: Pegasus Books Ltd. 2018

(4) Michael Burleigh, Young Saudi pretender’s days are numbered, The Times, 14 September 2018, https://www.thetimes.co.uk/article/young-saudi-pretender-s-days-are-numbered-hkhqs0239?shareToken=c5d15ffe552707d0f48ed75ea9978754

(5) Jamal Khashoggi, Opinion | Saudi Arabia's crown prince must restore dignity to his country — by ending Yemen's cruel war, The Washington Post, 12 September 2018, https://www.washingtonpost.com/news/global-opinions/wp/2018/09/11/saudi-arabias-crown-prince-must-restore-dignity-to-his-country-by-ending-yemens-cruel-war/

(6) Reuters, Lebanon's Hariri in Riyadh for first time since crisis, 28 February 2018, https://www.reuters.com/article/us-saudi-lebanon-hariri/lebanons-hariri-in-riyadh-for-first-time-since-crisis-idUSKCN1GC0GO

(7) Sinéad Baker, The full timeline of Canada and Saudi Arabia’s escalating feud over jailed human rights activists, Business Insider, 24 August 2018, https://www.businessinsider.sg/timeline-of-canada-saudi-arabia-diplomatic-feud-over-human-rights-2018-8/?r=US&IR=T

(8) James M. Dorsey, Tackling Corruption: Why Saudi Prince Mohammed’s approach raises questions, The Turbulent World of Middle East Soccer, 25 November 2017, https://mideastsoccer.blogspot.com/2017/11/tackling-corruption-why-saudi-prince.html

(9) United Nations Human Rights Council, Report of the Special Rapporteur on the promotion and protection of human rights and fundamental freedoms while countering terrorism on his mission to Saudi Arabia, 6 June 2018, https://www.ohchr.org/Documents/Issues/Terrorism/SR/A.HRC.40.%20XX.Add.2SaudiArabiaMission.pdf

(10) Reuters, Exclusive: Saudi king tipped the scale against Aramco IPO plans, 27 August 2018, https://www.reuters.com/article/us-saudi-aramco-ipo-king-exclusive/exclusive-saudi-king-tipped-the-scale-against-aramco-ipo-plans-idUSKCN1LC1MX

(11) Amir Tibon, Saudi King Tells U.S. That Peace Plan Must Include East Jerusalem as Palestinian Capital, Haaretz, 29 July 2018, https://www.haaretz.com/israel-news/saudis-say-u-s-peace-plan-must-include-e-j-l-as-palestinian-capital-1.6319323

(12) Saudi Vision 2030, 25 April 2016, http://vision2030.gov.sa/en

(13) Jennifer Gnana, A delay in Aramco IPO is in the interest of the Saudi energy industry, The National, 30 August 2018, https://www.thenational.ae/business/energy/a-delay-in-aramco-ipo-is-in-the-interest-of-the-saudi-energy-industry-1.764973

(15) Dasha Afanasieva, Saudi sovereign fund PIF raises $11 billion loan: source, Reuters, 24 August 2018, https://www.reuters.com/article/us-saudi-aramco-ipo-loan/saudi-sovereign-fund-pif-raises-11-billion-loan-source-idUSKCN1L90WK

(16) Summer Said and Rory Jones, Aramco Fights $70 Billion Price Tag for Saudi Chemicals Giant, The Wall Street Journal, 12 September 2018, https://www.wsj.com/articles/aramco-argues-over-right-price-for-sabic-1536765506

(17) Karen E. Young, Saudi Arabia’s Problem Isn’t the Canada Fight, It’s Capital Flight, Bloomberg, 17 August 2018, https://www.bloomberg.com/view/articles/2018-09-16/trump-needs-allies-for-the-great-u-s-china-trade-divorce

(18) Wael Mahdi, Saudi Aramco turns to tech to power future of oil, Arab News, 8 September 2018, http://www.arabnews.com/node/1368991

(19) Agence France Press, With Aramco IPO shelved, Saudi Arabia's PIF looks to tech, mega city, 5 September 2018, https://www.arabianbusiness.com/energy/403634-with-aramco-ipo-shelved-saudi-arabias-pif-looks-to-tech-mega-city-projects

(20) Ibid. Young, Saudi Arabia’s Problem

(21) Stephen Grand, Saudi's Vision 2030 Continues to Solicit Concerns, Atlantic Council, 11 September 2018, http://www.atlanticcouncil.org/blogs/menasource/saudi-s-vision-2030-continues-to-solicit-concerns

(22) The Economist, Transcript: Interview with Muhammad bin Salman, 6 January 2016, https://www.economist.com/middle-east-and-africa/2016/01/06/transcript-interview-with-muhammad-bin-salman

(23) United States District Court Southern District of New York, Plaintiffs v Kingdom of Saudi Arabia, 20 March 2017, https://static1.squarespace.com/static/57fbbfa88419c2de35c1639d/t/58d03556ff7c50abde86720f/1490040171270/Ashton-v-KSA-2017.pdf

(24) Ali Harb, The 9/11 lawsuit looming over Saudi Arabia's ambitions, Middle East Eye, 11 September 2018, https://www.middleeasteye.net/news/analysis-911-lawsuit-looms-over-saudi-arabias-economic-and-political-plans-1232597998

(25) House of Representatives Judiciary Committee, Bipartisan Lawmakers Applaud the Introduction of NOPEC Legislation, 24 May 2018, https://judiciary.house.gov/press-release/bipartisan-lawmakers-applaud-the-introduction-of-nopec-legislation/

(26) Jack Detsch, Saudi Arabia hires star lawyer to fight anti-oil cartel bill, Al-Monitor, 13 September 2018, https://www.al-monitor.com/pulse/originals/2018/09/saudi-arabia-hire-lawyer-oil-bill.html

(27) Adam Vaughan, FCA's rule change to lure Saudi Aramco prompts criticism, The Guardian, 8 June 2018, https://www.theguardian.com/business/2018/jun/08/fca-rule-change-to-lure-saudi-aramco-prompts-criticism

(28) Lucy Burton, MPs grill City watchdog on Saudi Aramco game plan, The Telegraph, 8 September 2018, https://www.telegraph.co.uk/business/2017/09/08/mps-grill-city-watchdog-saudi-aramco-game-plan/