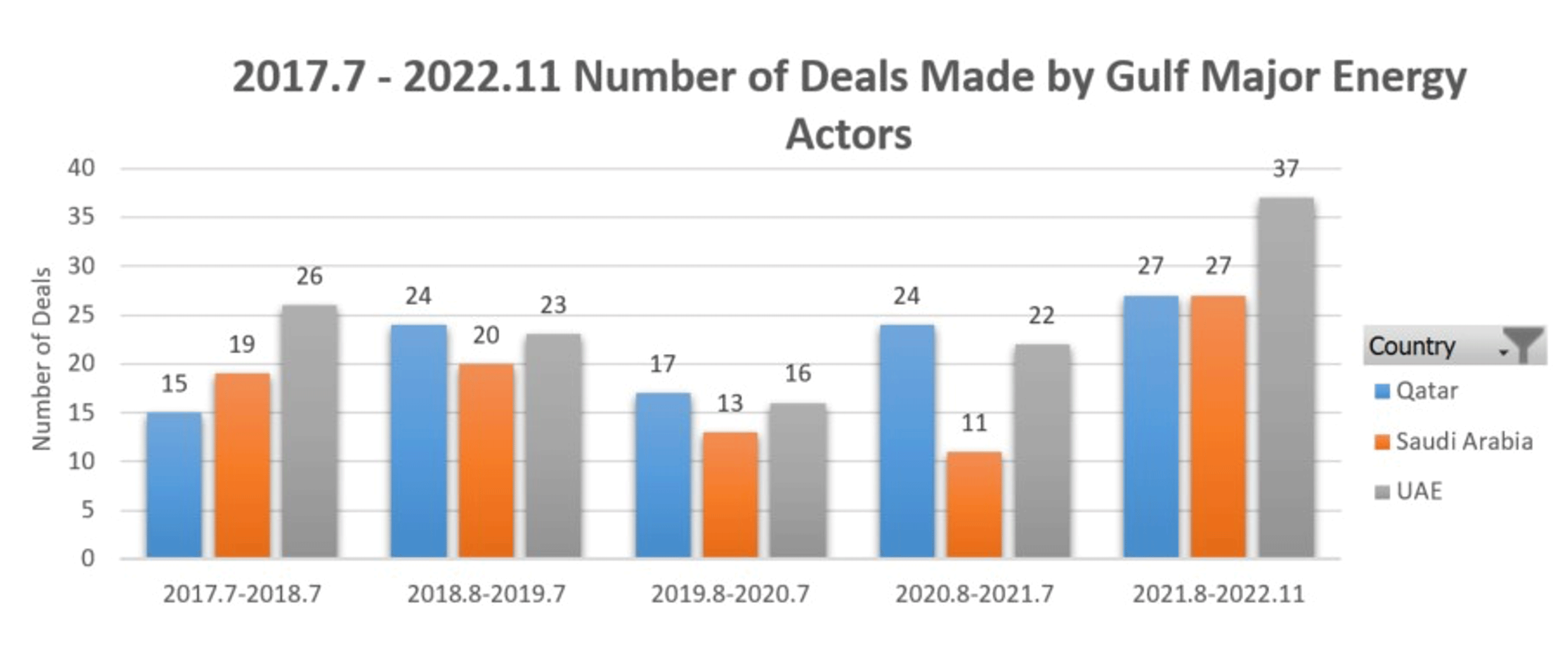

In recent months, the Ukraine war has underscored the centrality of the debate on national and regional energy strategies to global economic and geopolitical security as well as the climate crisis. This paper looks at how three of the major Gulf energy actors – Saudi Arabia, Qatar and the United Arab Emirates – have reacted to the pressures of recent geopolitical developments as well as the longer-term trend of the global shift towards cleaner energy. There are precedents for state actors, including Gulf actors, to focus in on the renewable energy sector as part of wider energy efforts during periods of uncertainty and instability across the international system. However, since mid-2021, all three Gulf actors examined here have been much more active across the entire energy sector compared to any single year since the breakdown of intra-Gulf relations and the launch of the embargo of Qatar in 2017. (See Figure 1.)

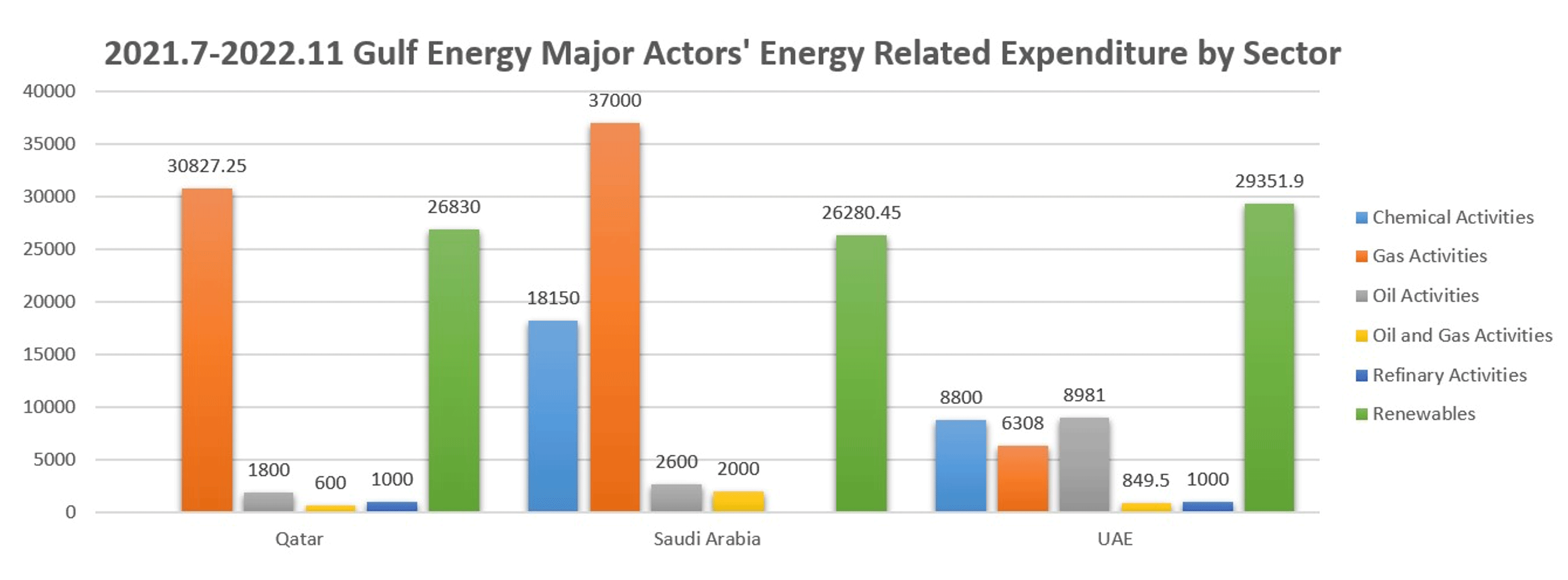

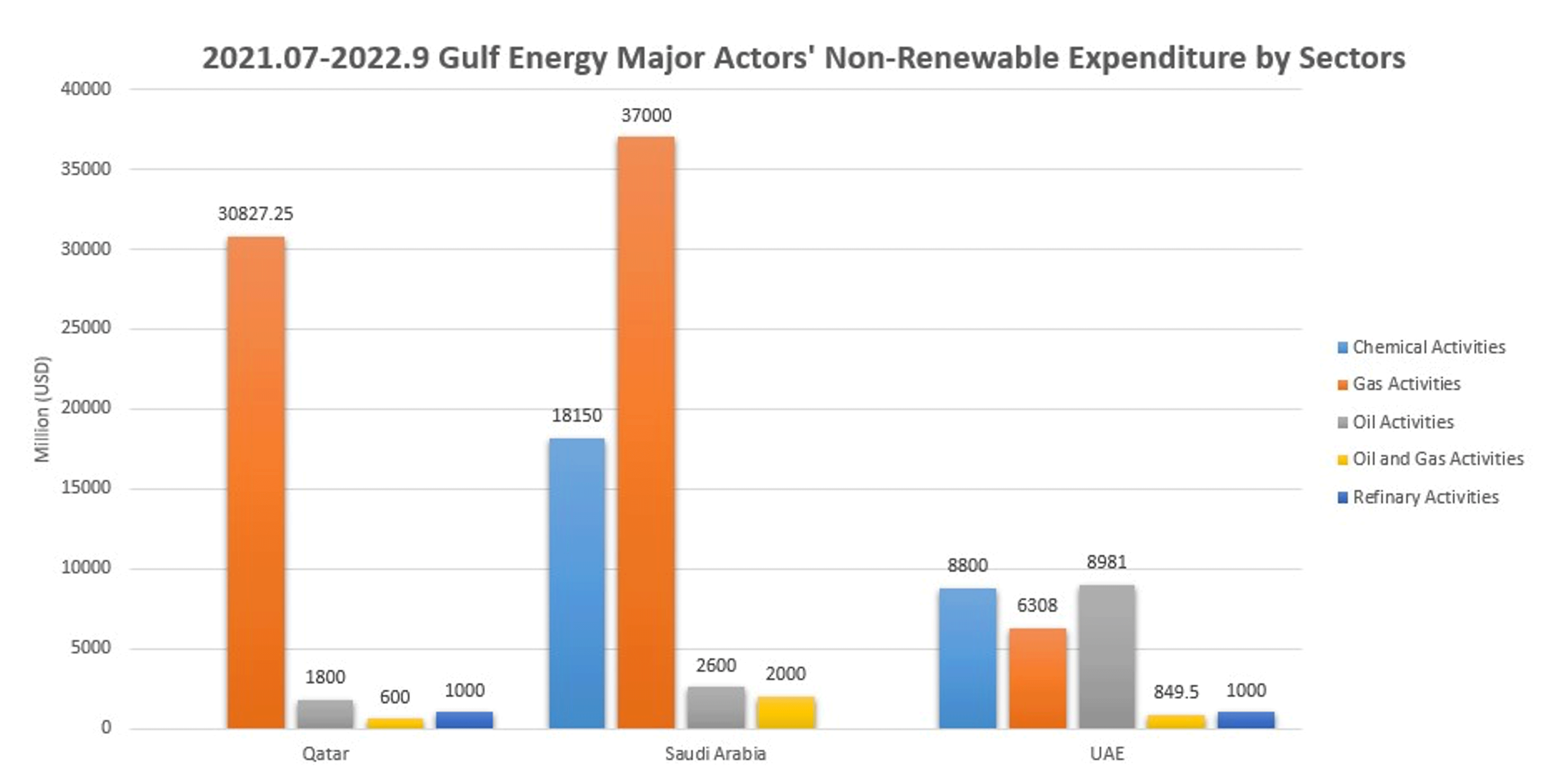

Breaking down these activities further by sector between July 2021 and November 2022 (see Figure 2), all three energy actors made significant investments in both the gas and renewable sectors.

In the years immediately preceding this rising activity, Qatar and Saudi Arabia made some large-scale domestic investments in renewables. Notably, in November 2018, Saudi Arabia financed its first solar project in Sakaka with a capacity of 300MW. (2) Meanwhile, in 2019, the first utility-scale wind farm in the Middle East, the Dumat Al-Jandal wind farm, was developed for the kingdom with a capacity of 400MW by Masdar and EDF Renewables.(3) In October 2019, the CEO of QatarEnergy, Said al-Kaabi, announced plans to capture and sequester 5 million tonnes of carbon dioxide from its LNG export facilities by 2025. (4) The following January, Qatar contracted French oil major Total and Japanese conglomerate Marubeni to build Qatar’s first utility-scale solar PV project (800MW) which came online in time for the November 2022 FIFA World Cup. (5)

In contrast, with the exception of the 2013 Shams 1 solar farm whose capacity is 300 MW (6) and the second phase of the Mohammed bin Rashid Al Maktoum Solar Park commissioned in March 2017 with a capacity of 200 MW, (7) the majority of the UAE’s involvement in renewables in the period prior to recent activity was overseas rather than domestically. For instance, the UAE invested in one waste-to-energy facility in Australia; one solar plant in each of Mauritania, Egypt and Jordan; and wind farms in the United Kingdom, Montenegro, the United States, Serbia and Oman. Nevertheless, even though the UAE was much more active overseas in this sector relative to Qatar and Saudi Arabia prior to 2020, Emirati investment in renewables still only accounted for approximately 3 percent of its total energy investment in this period. (See Figure 3.)

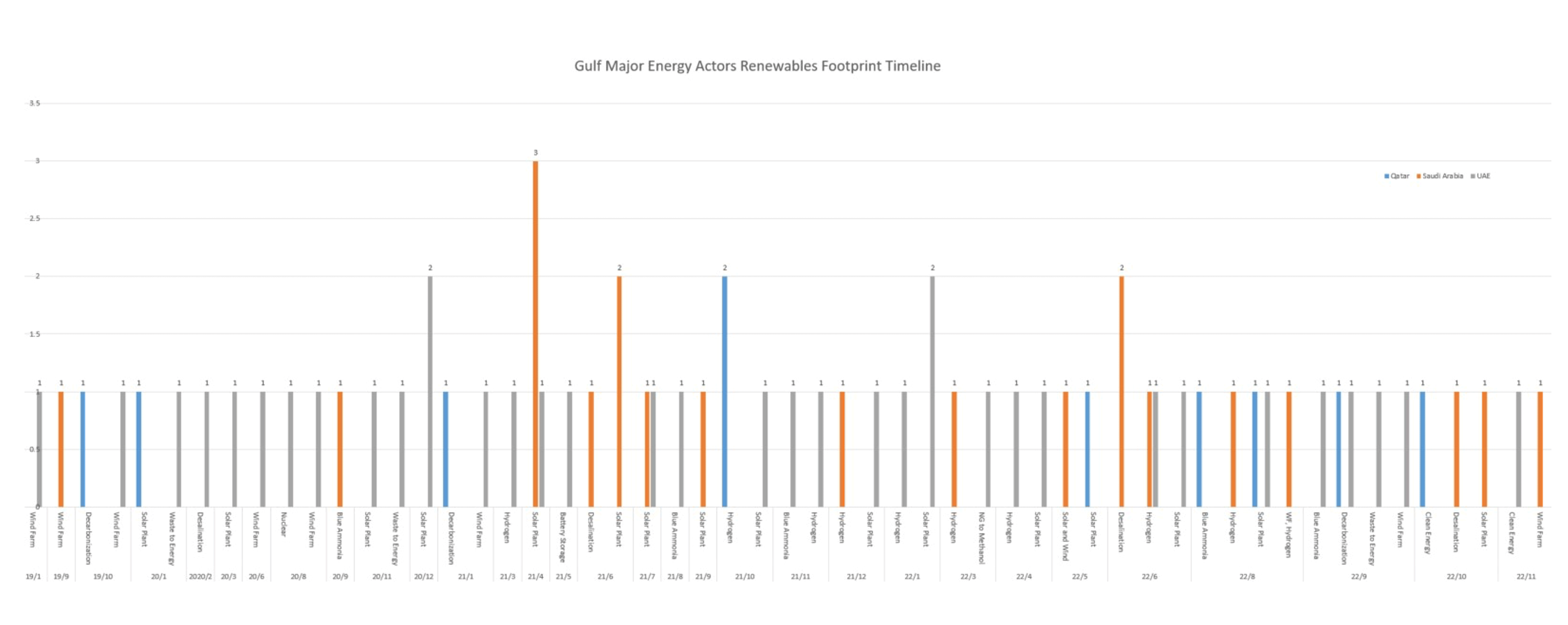

Since mid-2021 there has been a noticeable increase in the number of renewable projects and the size of relative investment in all three countries. From a base of only approximately 3 percent of its total energy expenditure prior to 2020, between July 2021 and November 2022, the UAE launched 8 major solar plant projects, one natural gas-to-methanol project, one waste-to-energy project, one wind farm, three blue ammonia projects, four hydrogen projects and one decarbonisation initiative. Most recently, during November 2022, the UAE and the US agreed to collaborate on clean energy projects globally with the goal of adding 100GW at a cost of US $100 billion by 2035. (8)

Saudi Arabia went from a base of nearly zero renewable investment before November 2018. However, in the period between April 2021 and November 2022, it invested in eight solar plants, five hydrogen projects, three sustainable desalination projects, one solar and wind power plant, two wind farms and hydrogen projects. In August 2022, the kingdom announced a further plan to develop three renewable energy projects at a cost of US $10 billion in Uzbekistan. The following November, the kingdom agreed to build a 10GW wind farm in Egypt.

Over this same time period, Qatar built on its previous endeavours by launching two more solar plant projects, two hydrogen projects and one project in each of the areas of decarbonisation and blue ammonia, as shown in Figure 4.

In terms of the value of these projects in relation to the countries’ overall investments in all energy projects, comparing the period between 2017 and 2019 with the period between mid-2021 and late 2022, Qatar increased its investment in renewables from 2% to 8% of overall energy investment. Renewables rose from 0% to 25% of total Saudi energy investment, whilst in the case of the UAE, they rose from 3% to 43% of all energy investment. (See Figure 3.)

The first explanation for this unprecedented move into the renewables sector is that these three Gulf energy actors are simply aligning themselves with global trends that are increasingly focused on addressing climate change priorities by transitioning to renewable energy. (9) In January 2021, Qatar announced plans to build out capacity for carbon capture and storage to 7 million tonnes per year by 2030. The following August, QatarEnergy announced its intention to reduce its Greenhouse gas (GHG) emissions by 25 percent by 2030. (10) In March 2022, QatarEnergy further announced its plan to achieve a reduction of 11 million tonnes of carbon dioxide per year by 2035. (11) For its part, in the final months of 2021, Saudi Aramco awarded contracts worth US $10 billion for the development of the vast Jafurah field as part of its goal of producing half of its electricity from gas and half from renewables in accordance with its 2060 net-zero target. The following month in December 2021, the Abu Dhabi National Oil Company (ADNOC) announced its intention to expand carbon dioxide capture to 5 million tonnes per year by 2030. (12)

These are some of the very public announcements in recent times that reflect the goals set down in the relevant strategic vision documents of all three Gulf states. One of the pillars of Qatar’s Vision 2030, which was published in 2008, is the “Management of the environment such that there is harmony between economic growth, social development and environmental protection.” (13) Since 2015, Qatar has aligned the outcomes and goals of its National Development Strategy with the goals of the United Nations’ (UN) Sustainable Development Agenda. Of the 247 goals set by the UN, Qatar has managed to align with 199. Qatar’s sustainability targets include installing 2 to 4GW of solar power energy and to have 10% of all motor vehicles electric by 2030. (14)

For its part, Saudi Vision 2030, which was announced in 2016, prioritises sustainable social, economic and environmental development. It is committed to Saudi investment in at least 9.5GW of renewable energy by 2030 as part of its ongoing move out of fossil fuels and in support of wide-ranging economic diversification plans. In order to offset the environmental impact of these considerable development ambitions, this vision also planned to launch more than 35 renewable projects across the kingdom by 2030. UAE Vision 2021 and Dubai’s Vision 2030, published in 2010 and 2016 respectively, include sustainable development as a major pillar. According to a report by the influential US-UAE Business Council, these visions form part of a wider Emirati plan to ensure that renewable energy accounts for a significant proportion of the country’s energy stock by 2050. (15)

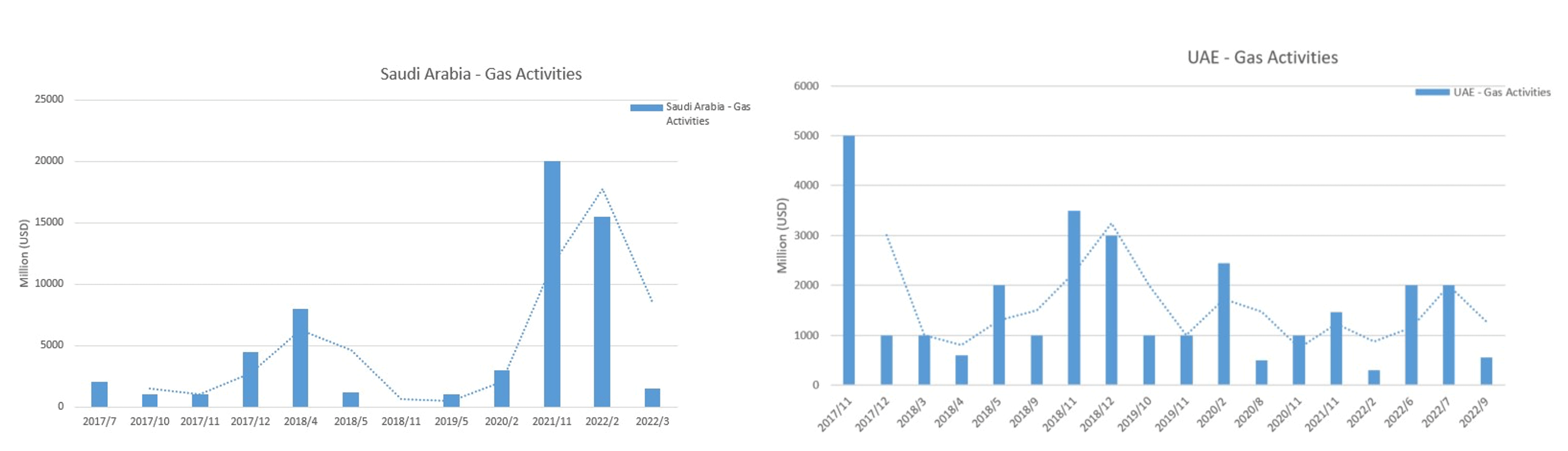

This extensive re-focusing on renewables can also be regarded as one more component of the wide-ranging competition between Gulf actors across many geopolitical and economic fronts. For example, as indicated in Figure 5, during the first year of the blockade of Qatar between June 2017 and June 2018, both Saudi Arabia and the UAE, the two leaders of the embargo, made significant increases in their investments in the natural gas and LNG sectors. In the Saudi case, this occurred in the half year between July 2017 and May 2018; and, in the case of the UAE, it began in November 2017 and continued at high levels over the following two years.

Such heavy spending in these sectors during the most intense period of the embargo of Qatar was born out of desire to reduce gas dependence on Qatari LNG, especially at a time when Qatar used its ongoing supply of gas to embargoing states to demonstrate its conciliatory and responsible position. But it also represented a decision, at the time, to challenge Qatar’s status as the leading regional actor in natural gas and LNG.

Interestingly, once the embargo “normalised” somewhat in its latter stages, investment in LNG by both Saudi Arabia and the UAE declined, only to rise significantly once again when the embargo ended following a meeting of Gulf leaders in Saudi Arabia during January 2021. It is possible to explain this development not only in terms of the end of the blockade but also as a response to the growing emphasis being placed on the move towards cleaner energy from 2021 onwards.

The end of the embargo of Qatar in early 2021 and the significant move into renewables subsequently served to intensify energy competition between Saudi Arabia, the UAE and Qatar. All three have looked to establish themselves as the dominant regional player or challenge the dominance of the others in various parts of the wider renewable energy sector. Such intra-regional competition is only a secondary driver of the move into renewables. Nonetheless, it is worth considering in the rapidly changing energy environment.

In June 2021, the CTO of Aramco, Ahmad Al-Khowaiter, announced his company’s intention to “have a large share of the market for blue hydrogen.” (16) A little under a year later, in May 2022, Saudi Arabia also announced that it would build the largest green hydrogen plant in the Gulf in its hi-tech city of Neom. (17) The following October, the kingdom announced its further intention to become a hub for green minerals as part of its plans to become the dominant global hydrogen supplier. (18) In June 2022, the Saudis also announced plans for the construction of the world’s biggest solar thermal plant, intended to generate steam to make aluminium rather than produce electricity or enhance oil recovery. If this project comes to fruition, it should dramatically reduce Saudi Arabia’s carbon footprint and bring it closer to achieving its net zero goal by 2060.

However, it should be noted that over the last decade, Saudi Arabia has announced several proposals to invest in solar power that have not come to fruition. This includes a 2011 plan to invest $100 billion in expanding power generating capacity including a nuclear plant and 5GW of solar energy capacity by 2020. This target was not reached. In 2015, Saudi Arabia also announced the launch of its first solar-powered desalination plant in Al Khafji, but it only had a planned capacity of 15 MW. This was followed up in 2018 by the Saudi announcement of plans to build its first large-scale renewable energy project in Sakaka with a capacity of 300 MW. A number of other solar projects have been proposed by a variety of public and private sector actors in the kingdom over the years, underscoring the ad hoc and uncoordinated nature of the Saudi approach up until recent times. It should be noted, however, that during this same time period, construction did commence on a wind farm project at Dumat al-Jandal with a capacity of 400 MW. Meanwhile, in late October 2022, Saudi Aramco’s CEO launched a US $1.5 billion sustainability fund, one of the largest funds of its type globally, to invest in stable and inclusive energy transition technology. (19)

Qatar, on the other hand, is currently looking to establish itself as a dominant actor in solar plants and blue ammonia. In August 2022, Qatar announced it would build the world’s largest blue ammonia facility. (20) The following October, the country’s Emir, Sheikh Tamim bin Hamad Al-Thani, inaugurated the Al Kharsaah Solar Power Plant in Al Kharsaah. This plant, which covers 10 square kilometres and includes more than 1,800,000 solar panels, is the first in Qatar and one of the largest in terms of size and capacity in the region with a total capacity of 800 MW. It is intended to satisfy 10% of the country’s peak electricity demands.

The UAE has looked to take a lead across a number of renewables sectors. In August 2021, Dr. Sultan Ahmed Al Jaber, the Emirati Minister of Industry and Advanced Technology and ADNOC Group’s CEO, announced that the UAE’s would become “a regional leader in the production of hydrogen and its carrier fuels.” This, he continued, would be achieved through “the expansion of our capabilities across the blue ammonia value chain” as a way to develop a “legacy as one of the world’s least carbon-intensive hydrocarbon producers and support industrial decarbonisation with a competitive, low-carbon product portfolio.” (21) This statement in particular is notable for the way it sought to assert Emirati leadership across the renewable space. In accordance with these ambitions, less than three months later, in October 2021, the UAE announced plans to invest more than US $160 billion to become the first Gulf state to achieve net zero carbon emissions by 2050. (22)

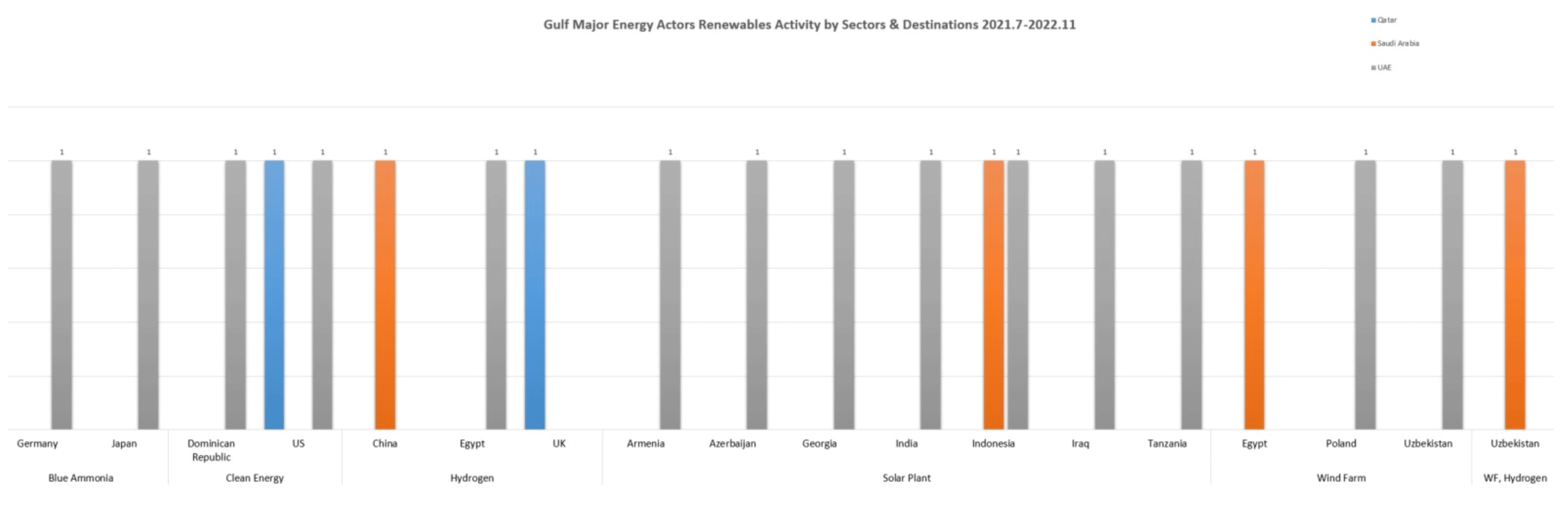

This rapid progress in developing the renewable energy sectors over the last year both in terms of the number of projects launched and the overall spend has not only taken place domestically. As shown in Figure 6, all three countries have also entered the renewables sector overseas. Qatar has invested in hydrogen projects in the UK and acquired a large holding in a major US clean energy company. Saudi Arabia has invested in hydrogen production and carbon capture in China, as well as one solar plant in Indonesia, one wind farm and hydrogen project in Uzbekistan and one wind farm in Egypt. Meanwhile, the UAE’s overseas renewables projects now include blue ammonia sales to Japan and Germany, two hydrogen projects, one each in the UK and Egypt, and three wind farms, one each in Poland, Uzbekistan and Egypt. It has also signed agreements for solar projects with Armenia, Georgia, Azerbaijan, Indonesia, Iraq, India and Tanzania and wind farm projects in Japan and Uzbekistan.

Conclusion

The major moves into the renewables sector between mid-2021 and late-2022 have not come at the expense of projects in the traditional areas of oil and gas. During September 2022, the President and CEO of Saudi Aramco, Amin bin Hassan Nasser, had a warning for those who “shame oil and gas investors, dismantle oil-and coal-fired power plants, fail to diversify energy supplies (especially gas), oppose LNG receiving terminals and reject nuclear power, your transition plan had better be right.” (23) QatarEnergy‘s CEO, Al-Kaabi, made a similar point in an earlier television interview in May 2022: “You can’t achieve this energy transition without fossil fuels and the best fossil fuel to mankind is gas.” (24) Subsequently, he expressed the view that “the best for the LNG industry is yet to come” and argued that more consumers are realising this vital fact. (25) To take one example in support of his position, according to the findings of a March 2022 Pew Research Center poll, while a majority of Americans support a move to carbon neutrality by 2050, only 31% think it is a good idea or realistic to phase out fossil fuels completely. (26)

It is also worth noting that recent moves into renewables are not only about addressing the climate crisis, meeting national targets for energy transition or competing with local rivals in new areas of energy. They must also be understood as a move that is driven by market forces as traditional customers are increasingly looking to import renewable energy alongside more traditional forms of fuel. Speaking at the LNG Producer-Consumer Conference in Japan in early October 2021, Al-Kaabi explained that “successful energy transition cannot be driven by producers alone. It is a shared responsibility that requires the active collaboration of energy producers, legislators and governments, and end-consumers.” (27)

In accordance with such arguments, in June 2020, the China National Offshore Oil Corporation (CNOOC) signed an agreement with Shell to become the first supplier to China of carbon-neutral LNG imports. The following September, Saudi Aramco announced a zero-carbon fuel value chain with Japan, alongside their first blue ammonia shipment to the country. The Japanese Ministry of Economy, Trade and Industry played a central role in backing the 40 tonne shipment of ammonia that followed. In August 2022, Shell announced that it would set up a joint venture in Shanghai, with the backing of Saudi Arabia, to build Asia’s first hydrogen distribution network. For its part, in August 2021 the UAE made 3 blue ammonia shipments to Japan. The following November, South Korea’s GS Energy agreed to import 200,000 tonnes of blue ammonia from the UAE. In September 2022, the UAE also completed its first shipment of low carbon ammonia to Germany.

Regardless of the different drivers behind these large scale moves into the renewables sector, these actions may well result in these 3 pro-active and ambitious Gulf states establishing themselves as hubs for renewable energy while they also look to consolidate their positions in the ever-changing oil and gas markets over the medium and long term. They have, in other words, not only increased their commitment to renewables as part of the expansion of their overall energy portfolios. They have, arguably much more importantly, set themselves on a path that may ultimately locate them at the heart of the new energy system in areas such as hydrogen and blue ammonia, like they did in the oil and LNG sectors over the last half century.

- This publication was made possible by a National Priorities Research Program Standard (NPRP-S) Twelfth (12th) Cycle grant # NPRP12S-0210-190067 from the Qatar National Research Fund (a member of Qatar Foundation). The findings herein reflect the work, and are solely the responsibility of the authors.

- “Sakaka Photovoltaic Solar Project”, Power Technology, 20 April 2021, https://bit.ly/3FL7Rvk (accessed 21 December 2022).

- “Dumat Al Jandal Wind Farm”, NS Energy, 22 November 2022, https://bit.ly/3YH9liY (accessed 21 December 2022).

- “Qatar building large CO2 storage plant”, Al Jazeera, 8 October 2019, https://bit.ly/3joaUSr (accessed 21 December 2022).

- John Parnell, “Total and Marubeni to Build 800MW Solar Plant in Qatar Ahead of World Cup”, Greentech Media, 21 January 2020, https://bit.ly/3VgOfVm (accessed 21 December 2022).

- “Shams 1 Solar Power Station Project”, Power Technology, 3 December 2013, https://bit.ly/3G99YdG (accessed 21 December 2022).

- “Mohammed bin Rashid Al Maktoum Solar Park”, https://bit.ly/3v8YUH7 (accessed 21 December 2022).

- “UAE and U.S. reach deal for $100 billion in clean energy projects”, Reuters, 2 November 2022, https://reut.rs/3FFP04K (accessed 21 December 2022).

- “Saudi Aramco Urges World Unity around New Energy Transformation Plan”, Asharq Al-Awsat, 21 September 2022, https://bit.ly/3jnMetD (accessed 21 December 2022).

- “Qatar- Energy Efficiency and Sustainability Initiatives – Carbon Footprint Reduction”, US International Trade Administration, 31 May 2022, https://bit.ly/3FLDhll (accessed 21 December 2022).

- Nishant Ugal, “QatarEnergy sets ‘aggressive target’ to scale up CCS and solar power by 2035”, Upstreamonline.com, 7 March 2022, https://bit.ly/3Veaiwc (accessed 21 December 2022).

- “UAE’s ADNOC, TotalEnergies sign agreement on CCS, hydrogen”, S&P Global Commodity Insights, 5 December 2021, https://bit.ly/3GjPpeV (accessed 21 December 2022).

- “Qatar National Vision 2030”, Government Communications Office, State of Qatar, https://bit.ly/3WhA3gb (accessed 21 December 2022).

- “Qatar Sustainability Report: A Leader in Green Initiatives”, US-Qatar Business Council, May 2021, https://bit.ly/3BRYcC7 (accessed 21 December 2022).

- ‘Transforming the Energy Mix: Renewable and Nuclear Energy’, US-UAE Business Council, 2022, https://bit.ly/3GbzoqY (accessed 21 December 2022).

- “Saudi Aramco bets on blue hydrogen exports ramping up’, PoliticoPro, 28 June 2021, https://bit.ly/3Ve3Kxt (accessed 21 December 2022).

- Vivian Nerein, ‘Saudi Arabia to Start Building Green Hydrogen Plant in Neom’, Bloomberg, 17 March 2022, https://bloom.bg/3WBYBQO (accessed 21 December 2022).

- “Saudi Arabia explores opportunities in South Africa to become global supplier of hydrogen”, Arab News, 4 October 2022, https://arab.news/5j9xf (accessed 21 December 2022).

- Jana Salloum, Fahad Abuljadayel and Dana Abdelaziz, “Aramco announces $1.5bn global sustainability fund”, Arab News, 26 October 2022, https://arab.news/ckead (accessed 21 December 2022).

- “QatarEnergy Renewable Solutions & QAFCO launch the world’s largest blue ammonia facility”, QatarEnergy News, 31 August 2022, https://bit.ly/3WxUeq7 (accessed 21 December 2022).

- Richard Ewing, “ADNOC and Fertiglobe sell UAE’s first cargo of blue ammonia to Japan’s Itochu”, Independent Commodity Intelligence Servers, 3 August 2021, https://bit.ly/3vakYBa (accessed 21 December 2022).

- Dan Murphy and Natasha Turak. “UAE receives praise and skepticism after revealing first net-zero pledge in the region”, CNBC, 7 October 2021, https://cnb.cx/3WCUdkS (accessed 21 December 2022).

- “Saudi Aramco Urges World Unity around New Energy Transformation Plan”, Asharq Al-Awsat, 21 September 2022, https://bit.ly/3jnMetD (accessed 21 December 2022).

- “Exclusive interview with H.E. Minister Al-Kaabi on Sky News”, YouTube, 26 May 2022, https://bit.ly/3YT5Shp (accessed 21 December 2022).

- Lydia Woellwarth, Qatar Petroleum CEO on the need for a collaborative approach for the energy transition’, LNG Industry, 7 October 2021, https://bit.ly/3HTuQqw (accessed 21 December 2022).

- Alec Tyson, Cary Funk and Brian Kennedy, “Americans Largely Favor U.S. Taking Steps To Become Carbon Neutral by 2050”, Pew Research Center Report, 1 March 2022, https://pewrsr.ch/3YFuPwx (accessed 21 December 2022).

- Lydia Woellwarth, Qatar Petroleum CEO on the need for a collaborative approach for the energy transition’, LNG Industry, 7 October 2021, https://bit.ly/3HTuQqw (accessed 21 December 2022).