Abstract

2018 was a significant year in terms of energy geopolitics: The United States once again was able to regain its title as the world’s largest producer of oil. For much of the 20th Century, the United States had been the world largest producer of oil and that dominance lasted until 1974 when it was overtaken by the Soviet Union at the height of the Cold War. The Soviets were subsequently passed by Saudi Arabia in 1976 – from that point onwards, it was the Saudis who were to dominate the oil market, which they have done for the last four decades. The manner, in which the United States overtook Saudi Arabia’s position, necessitates a broader consideration of the geopolitical change in the global energy markets, and what that means geopolitically in terms of US engagement with the Middle East.

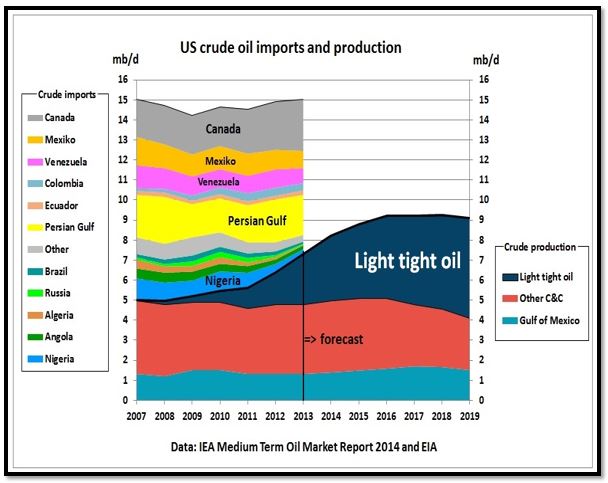

The exploitation of shale rock in the United States has been nothing short of revolutionary in the energy sector and this allowed the United States to inch ahead of Riyadh as the world’s largest producer of oil. The broader geopolitical implications of the shale revolution in the United States is that it has enabled “energy independence” to be achieved. Whilst global supply, demand and geopolitical risk all impacts the price of West Texas Intermediate (WTI) and Texas Sweet Light oil, which directly impact the US consumer, what is important here is that by the US achieving energy independence and becoming the world’s largest producer of oil, it has had an important psychological and political impact which has implications. The significance of this shift should not be underestimated, and will be considered here through the lens of US foreign policy and its strategic interests in the Middle Eastern region.

It was in 2018 that the eightieth anniversary of the discovery of oil in Saudi Arabia – 3 March 1938 - occurred and set in motion an evolution in US strategic thinking towards the Middle Eastern region. This crystallized during the Nixon administration, as 50 years ago in 1968, the announcement of the Nixon doctrine laid out a strategic design which placed primary emphasis on both ensuring the free flow of crude oil from the Gulf region and the support of regional allies against the spread of socialism from the Soviet Union. This strategy may have been devised at the height of the Cold War, yet US strategic interests in the region remained largely consistent from that point onwards.

The Nixon doctrine led to the establishment of the twin-pillars strategy towards Gulf security, which saw primary support being given to Iran, and to a lesser degree Saudi Arabia, as a means of catering for regional security through access to military equipment in addition to political and intelligence support. Both were the twin pillars, or twin policemen, who were supported to ensure the achievement of US strategic interests by proxy. While this strategy lasted until the Iranian revolution in 1979, despite change and upheaval in the geopolitical landscape which included the Iran-Iraq war (1980-88), Iraq’s invasion of Kuwait in 1990, and the U.S.-led invasion of Iraq in 2003; throughout this period, the United States maintained the strategic perspective that a free flow of oil from the Gulf region was a defining feature of its regional foreign policy.

Yet with the election of President Donald Trump, whose global foreign policy perspective has an isolationist character and one which is more ‘nationalist’ rather than ‘internationalist’ in its outlook, a changed context has emerged. Indeed, the emergence of the United States as the world's largest producer of oil and with that becoming energy independent, it is clear that the strategic calculations of the United States towards the Middle East, and in particular towards the Gulf region, has taken on a new context which can be expected to foster a new dynamic in US foreign policy.

|

| [Oil & Gas Journal] |

The central argument here is that the above factors of energy independence, coupled with a the dominate political value through the White House in nationalist isolationism, these mutually reinforcing factors which will further contribute towards a reluctance for the United States to seek an interventionist role towards the promotion of peace and security for the Gulf region. It should be recognized here that the prerogative to determine the foreign policy of the United States is the responsibility of the presidency, and this is enshrined in the constitution of the United States. On this basis, the broader significance of the United States emerging as the world's largest producer of crude oil in 2018 is that for the duration of the Trump presidency, and for the 2019 period, it can be expected that the reluctance for a political engagement with the Middle East, and within the Gulf region, can be expected only to widen further under a Trump presidency. In essence, it can be expected that for 2019, this pivot away from the United States proactively helping resolve regional insecurity will continue.

The Trump Presidency: From Strategic Interests to Transactional Calculations

When President Donald Trump took office as President of the United States in January 2017, regional leaders were mindful that throughout the presidential election campaign, he had been a vocal critic of President Obama and Secretary of State, Hillary Clinton. Based on the decisions that the Obama administration had made, the traditional allies of the United States not only saw that the United States had done a pivot to Asia, but it also pivoted towards Iran and had upset the regional balance of power. The policy decisions made by the Obama administration has served to undermine confidence that regional allies had in the United States as a steadfast partner.

Whilst the election of Donald Trump was divisive within the United States, the reaction in the region given his vocal opposition towards the Iranian nuclear deal and condemnation of Iranian proxies, within the context of his pro-Israeli stance, made him a welcome entrant to the White House to key regional partners such as Saudi Arabia who had been increasingly viewing themselves as locked in an existential struggle with Iran. Moreover, given his commercial background, there was every reason to expect that he could be a new partner. Great attention is traditionally given to the first country that a President of the United States chooses to visit after they are elected, and in the case of Trump, it was Saudi Arabia.(1)

There were two unique aspects about this inaugural visit, which should be identified here: the first was that a major arms deal was signed with Saudi Arabia which amounted to over US$350 billion and was heralded as the largest arms deal in history. This figure was certainly inflated due to it encompassing previously signed agreements, and it included intentions to buy rather than actual purchases, it was nonetheless a political accomplishment for Trump given he was elected on the platform of economic nationalism. The more important aspect of this inaugural visit was that an international summit was convened in Saudi Arabia where Trump could address the leaders of over 50 Arab and Muslim countries, with the notable exceptions being Iran, Syria, and Sudan.

In Trump's keynote address, he placed emphasis on regional states taking responsibility for "driving out" terrorism from their countries and reset the US position with the region as allowing each country to chart its political course, which was a definite departure from the idealist principles that have traditionally been in US foreign policy for democracy and freedom. The geopolitical implications of President Trump's summit meeting with the leaders and representatives of the majority of Arab and Islamic countries are several: it signaled US support for Iran being combated as an international pariah nation, which was a clear reversal of Obama's position of engagement with Iran. It also fed into the anti-Iranian geopolitical perspective which had been steadily rising in Saudi Arabia and its allies most notably since the fall of an Iraq and the Taliban in Afghanistan.

|

| [Resilience.org] |

Trump's position could be characterized as a strategic disengagement from the region, where the emphasis was given to the region to address its inherent challenges. The importance of this shift lies in the way the United States has historically been a major player in Middle Eastern geopolitics and the security guarantor to key Arab states. This translated to the United States playing a coordination role in the foreign policies of key hegemonic states such as Egypt and Saudi Arabia, and given the nature of the US security umbrella, combating the threat posed by Iran had been historically undertaken in cooperation with the United States.

Yet with Trump signaling the need for regional states to take a proactive and independent role in combating extremism, of which Iran and Syria were part of, his position had built on the successive impact previous US administrations have had in inflaming geopolitical tensions between the regional powers of Saudi Arabia and Iran, through essentially inviting Sunni Arab states to take on an independent foreign policy to achieve such goals. To put this in a historical context, Trump had signaled US disengagement from successive regional security strategies that dated back to President Richard Nixon. The importance of a new energy independence character only serves to add to this perspective.

Trump reiterated the view that the United States will no longer seek to promote its values on other countries; he stated, "I also promised that America would not seek to impose our way of life on others, but to outstretch our hands in the spirit of cooperation and trust." This position is significant in that it was a historical departure from the values of the United States was founded on as a country, and especially since the Presidency of Woodrow Wilson, values of democracy and freedom have been a key pillar of United States foreign policy, which although at times subordinated to national interest consideration, it has been nonetheless been fundamental part of US diplomacy. By making clear that these were no longer going to be a priority in US foreign policy, Trump essentially provided regional leaders no additional incentive to address the underlying political challenges which had sparked the region-wide uprising in 2010-11. Indeed, such disengagement from global affairs, which can be understood as isolationism, was something which had not been experienced in the United States since the 1930s in the aftermath of the Great Depression.

Geopolitically for the region, the consequence of Trump's position is the way he had disengaged the United States from orchestrating or promoting a concept of regional order. The restraints on countries such as Saudi Arabia were thus lifted, and its priorities were to become a defining feature in regional geopolitics as part of its national security strategy calculations, which essentially translated to a sharpened focus against the Iranian axis through proxy conflict, and an aggressive zero-sum foreign policy calculation that manifested in the ongoing siege of Qatar.

The significance of the above in relation to energy is therefore that energy independence is serving to fuel a transactional perspective by the Trump presidency in its foreign-policy calculations towards the Middle East, and the Gulf region in particular. Indeed, US energy independence serves to lower US strategic interests in the Gulf region and therefore serves to support transactional foreign policy approach rather than a strategically grounded one. More broadly, this is a wider pattern, which feeds into the foreign-policy calculations of the United States within the broader Middle East region.

|

| [Business Wire] |

Political Economy Challenges Posed by Energy Developments

For energy exporting countries, whose national economies draw a significant proportion of their gross domestic product (GDP) from such exports, the changing nature of the global energy market has special importance. Over the last decade, the global energy market has gone through a rapid transformation. The emergence of the United States as the world’s largest producer of oil, in addition to becoming an exporter of natural gas, has heralded a new era whereby the United States has achieved energy independence.(2) The implications of this are significant in that it signals a shift in the manner in which national security and economic interests of the United States are calculated. The impact of this can be understood as a new era away from the security of natural resources are playing an important role in foreign policy calculations, which has been a central feature of US engagement with the Middle East region since the end of the Second World War. The emergence of the United States as a major player in the global energy market also heralds greater supply and competition. This has been driven through the exploitation of shale in the United States and has served to have a dampening effect on global prices for oil. The key beneficiary of this has been major energy-importing countries such as China, as cheaper oil has fueled economic growth and dulled inflation.

With the United States emerging as a net exporter of liquefied natural gas, its export capacity will be helping grow the global LNG market which feeds into Qatar’s overall strategy for enhancing the adoption of LNG on a global level. Based on the United States’ geographical location, the 2016 completion of a widening of the Panama Canal, has greatly facilitated the ability for the U.S. LNG exporters to have a global reach and the supply.(3) The US$5.3 billion expansion of the Panama Canal has reduced the transit cost from the United States and also the duration by a third. Shipments to China can now be completed in 14 days which allows both U.S. West Coast and Gulf Coast produces to be competitive in their supply to China given its role as the main growth market for LNG globally.(4)

|

| [International Energy Agency] |

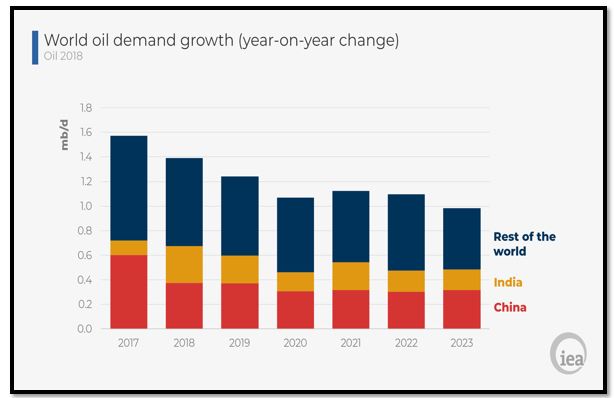

Whilst the changing fortunes of the United States has certainly had a global impact, a broader pattern that can be observed is that there is a shift in the center of gravity for energy demand at a global level, and this is primarily characterized by the move in demand from OECD to non-OECD nations, with particular emphasis on China and India. This shift in demand has been a trend since the 1990s and has been driven by rising levels of economic prosperity of billions of people in developing countries.(5) Given the size of China and India’s population, they have proven to be the largest drivers in global demand for oil between 2007 to 2017.

In terms of natural gas, it is China which has proven to be the largest driver of demand over the last decade, and this trend is projected to continue. Yet at a geopolitical level, it is important to recognize that south and northern East Asia constitutes the majority of global demand in natural gas. The combined demand from China, Japan, South Korea, and India, constitute more than sixty percent of global demand. It is based on this that these markets will necessarily hold a special importance for Qatar and other leading LNG suppliers, in its terms of both current and future market demand.

Although it is clear that there has been a shift in the center of gravity in demand from OECD to non-OECD nations, it is important to recognize that supply of LNG is also growing. Australia has emerged as a leading producer of LNG and has in 2018 exported a comparative amount to that of Qatar, which is the world’s leading producer. While Qatar’s gas supplies from non-associated natural gas fields, in the case of Australia, it is from coal-seam gas and has been enabled by significant investment into the sector during a period of high oil prices. Whilst some predictions had indicated that Australia would overtake Qatar as the world’s leading producer, Qatar announced in September 2018 to increase its LNG output (at 77 million tons per year in 2018) to 110 million by 2024. This is despite a parallel growth in global LNG output globally.

|

| [Gulf Daily News] |

Overall, 2019 promises to see this trend in the demand and supply dynamics continue. The main conclusion that can be drawn from this is that a progressive integration between the Arab Gulf states with south and east Asia will continue, driven by energy. In particular, this heralds greater engagement with China and a growth in the strategic importance of China within the Gulf region. This is all the more poignant given the existing and growing isolationism coming from the United States. Indeed, it is on this basis that diplomatic and commercial engagement with China can be expected to accelerate during 2019 given these contextual forces.

The Future of OPEC?

As 2018 drew to a close, many analysts were taken by surprise as Qatar announced that it was withdrawing from OPEC. Qatar had been an early member of the organization yet it always was a marginal player in terms of its oil export capacity. Founded in 1960, OPEC was established by five states: Iran, Iraq, Kuwait, Saudi Arabia and Venezuela. Beyond the initial five founding member states, Qatar was the first country to voluntarily join this organisation in 1961 after its establishment. In the years that followed, a wave of countries also joined which included Libya, United Arab Emirates, Algeria and Nigeria amongst others. Given Qatar had been a member for 57 years, its decision proved as a surprise to many international observers of the energy sector, yet it should not have done given the way in which Qatar's energy strategy had been steadily evolving and in particular the manner in which Qatar was seeking to develop the liquefied natural gas sector. Indeed, the decision to withdraw from OPEC is, therefore, a natural evolution of Qatar`s vision for its energy sector and how it engages globally. It is important to appreciate that the role of OPEC in Qatar’s energy strategy was a legacy of an older era, when Qatar did not have a natural gas industry to rely on.

|

| [OPEC Annual Statistical Bulletin 2018] |

Qatar’s crude oil exports amounted to around 600K barrels per day in 2017, which was a modest 2% of OPEC’s total output. However, the value of OPEC to its member countries has been progressively waning for some time. A recent example was in May 2017, when OPEC announced that it was extending its output cuts of 1.8 million barrels per day, by nine months until the first-quarter of 2018. Such was the lackluster impact of OPEC’s announcement; the market reaction saw oil process fall by around 4% - a far cry from its heyday when it could cause a spike in crude oil prices with the mere threat of a stroke of a pen on export quotas.

OPEC remains essentially a Saudi-led cartel, with less global relevancy given the shale revolution. The exploitation of Shale has allowed the United States to overtake Saudi Arabia as the world’s largest oil producer. While Saudi Arabia’s ability to manipulate the market through OPEC has certainly weakened, the future for OPEC necessitates Russian support for it to deliver on its promises. It is, therefore, the Saudi-Russian oil axis that matters for OPEC, which means smaller oil producers have even less room to influence decisions.

The future of OPEC for 2019 should be understood within the context of the rising concern on Saudi Arabia that is growing in the United States congress, following the premeditated murder of Saudi journalist Jamal Khashoggi in Istanbul. Such sentiment makes it more likely that the US congress may adopt antitrust legislation – the NOPEC Act, which will open the doors to litigation against Arab and non-Arab member states of OPEC. Indeed, if this were to happen, the price of oil can be expected to have downward pressure.

The 2019 Outlook: Energy Induced Political and Economic Uncertainty

In the final analysis, it is clear that the role of energy has had a clear impact on both geopolitics and economics during 2018, and that this can be expected to be the case in 2019. From a strategic perspective, the relationship of the United States with the region is in a period of change and that is being impacted by the changing energy landscape at a geopolitical level. This has implications not only in terms of regional stability, but also in terms of how key states within the region conduct their foreign policy. Indeed, such change is having an impact on the regional security architecture and this underlines the need for a new definition of regional order to be developed.

It is also striking that given the hostility to which Saudi Arabia is being viewed by members of the United States Congress, the central pillars on which energy geopolitics in the Middle East have been shaped have now entered a new phase which can be viewed as the most challenging historically since United States’ strategic interests in the region crystallized during the Nixon administration. The extraordinary criticism and scrutiny that Saudi Arabia is now under holds the potential for the United States Congress enacting legislation against OPEC. Anti-trust legislation against OPEC would have a turbulent impact on the global energy market in that such pressure could lead OPEC members withdrawing from the organization. Whilst it is unclear if this will take place during 2019, one could speculate that if it were to happen, it would have a significant and disruptive impact on the global price of oil. In the absence of OPEC, oil export quotas would no longer be applied; and thus downward pressure on the global price of oil would grow.

|

| [Rystad Energy] |

The challenge of a lower price of oil however is that it has a direct impact on the economies of the Arab Gulf states, and some are more vulnerable than others. Despite its oil reserves, the challenge Saudi Arabia faces is largely a product of the way its political economy has evolved. A key driver of Saudi Vision 2030 is based on the recognition that an economic transformation is needed given the unsustainability of economic system in the country. Oil revenue has certainly allowed for infrastructural development, yet with the global downturn in oil prices from 2014, in addition to technological transformations in the way in which oil can be extracted, poses the challenge of a depressed oil market.

One observation that despite the fluctuations in the price of oil, it is possible to identify at least four such market cycles: from 1973 to 1985, the price of crude oil was in a high price cycle lasting for 12 years. A second cycle took place from 1986 to 2000, where a low-price cycle occurred for 14 years. The third cycle in oil prices can be identified from 2001 to 2014, which is 13 years of high oil prices. It was the downturn in 2014 which can be understood here as the start of a new cycle of low oil prices.

Ultimately, it is the market dynamics of having high oil prices which allows for greater investment in the oil industry to take place in for new markets to be uncovered. However, one of the key differences in the current cycle is the advent a new age in oil and gas exploitation through deposits of shale rock. This fact allowed the United States to become increasingly energy secure and to position itself as an oil and gas exporter; but, it is given the commercial viability of shale producers which acts as a depressant on global oil prices: the higher the price goes, the more commercially viable it is for producers to exploit Shale and therefore greater production of oil leads to depression of prices. Therefore, the new energy landscape serves to depress prices for the foreseeable future which has clear implications on the Arab Gulf region.

1) Al-Rasheed, M. (2017). "Trump and Saudi Arabia: Rethinking the relationship with Riyadh." Foreign Affairs.

2) Grigas, A. (2017). The new geopolitics of natural gas. Harvard University Press.

3) Wright, S. (2017). Qatar's LNG: Impact of the Changing East?Asian Market. Middle East Policy, 24(1), 154-165.

4) Moryadee, S., Gabriel, S. A., & Avetisyan, H. G. (2014). Investigating the potential effects of US LNG exports on global natural gas markets. Energy Strategy Reviews, 2(3-4), 273-288.

5) Grigas, A. (2017). The new geopolitics of natural gas. Harvard University Press.